Chart of Accounts(COA) for Small Business

COA_for_Small_Business.mp4

If “Chart of Account” sounds intimidating, please don’t! What if you could set up your financial system in just 10 minutes and have it practically run itself?

So What Exactly is a Chart of Accounts?

Think of your COA as the master list of labels you use to sort every dollar that comes into or goes out of your business. Imagine a set of digital folders where every transaction has a home. This organization is essential for generating accurate financial reports like a Profit & Loss (P&L) statement or a Balance Sheet.

Your COA is typically organized into six main categories:

Assets: Everything your business owns.- Cash in the bank

- Inventory

- Equipment.

Liabilities: Everything your business owes.- Credit card balances

- Loans

- Sales tax payable.

Equity: The net worth of your business.- Investment

- Retained profits.

Income: All the money you earn from sales or services. Also called as Revenue.Cost of Goods Sold (COGS): Direct costs of producing your product or service.- Raw materials

- Marketplace fees.

Expenses: The costs of running your business.- Rent

- Software subscriptions

- Marketing.

Keep It Simple: Names Beat Numbers

There are certain circumstances when you need to fine-tune COA numbers. If so, please talk to accountant or our support team!

A common question is whether you need complex account numbers for your COA. For most small businesses, the answer is a simple no. Clear, short names are more readable and easier to manage. The goal is to create fewer, clearer buckets for your money, which leads to faster bookkeeping and cleaner reports.

You can always add more accounts later, but it’s best to start small and only add a new category when you truly need it for a report.

A Starter COA for Your Business

Wesley Ledger comes with default set of COA for you, but you can customize it if you want.

Every business is unique, but most can start with a clean, basic COA. From there, you can tailor it to your industry.

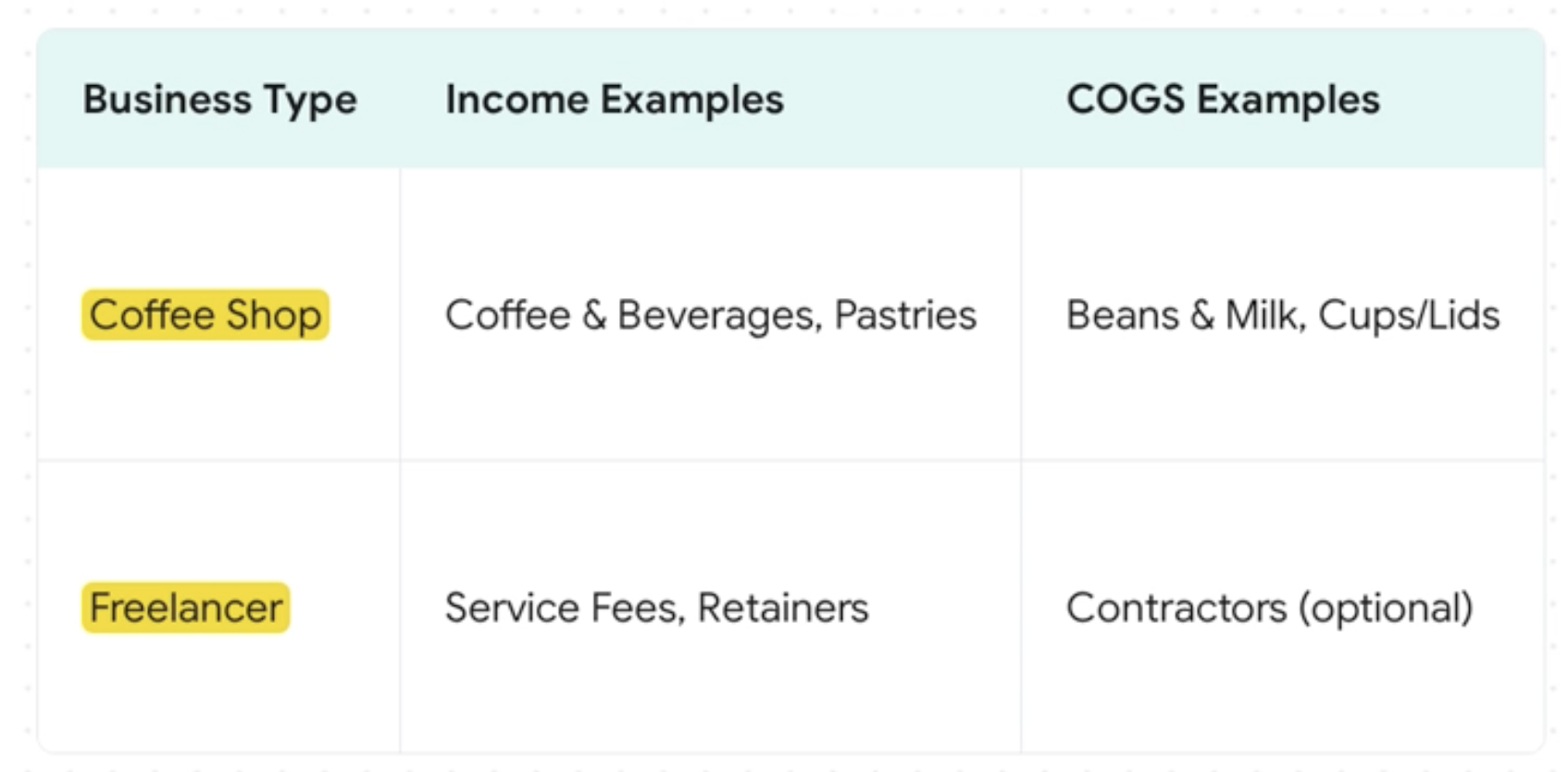

- A Coffee Shop might have income accounts like "Coffee & Beverages" and "Pastries," with COGS accounts for "Beans & Milk" and "Cups/Lids".

- An E-commerce Store will use "Online Store Sales" for income and "Inventory Purchased" and "Marketplace/Merchant Fees" for COGS.

- A Freelancer may only need income accounts for "Service Fees" and "Retainers," with expenses for "SaaS Tools" and "Travel & Meals".

The key is to use short, clear names that make sense for how you operate.

Let Software Do the Heavy Lifting

You can expect more than 95% of your transactions to be categorized automatically

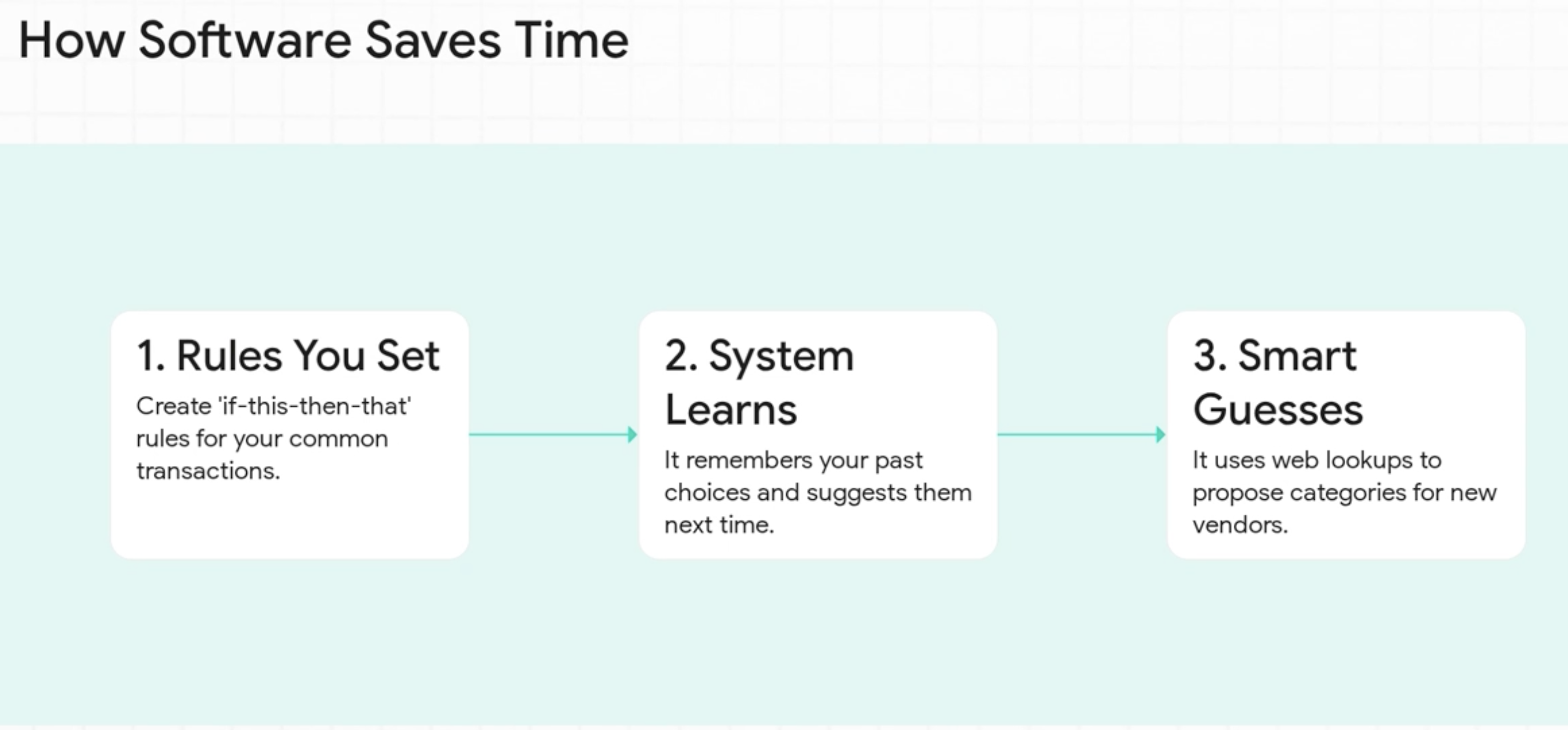

A well-organized COA is the foundation, but modern bookkeeping software is what saves you time. It should help you automate most of the categorization so you only have to review the exceptions. Look for features that:

- Use Rules You Control: Set up simple "if-this-then-that" rules for recurring transactions. For example, a rule could automatically categorize any payment to "Meta/Facebook Ads" as a "Marketing/Ads" expense.

- Learn from Your Choices: Good software remembers how you categorize a transaction. If you classify a payment to "GAS STATION ABC" as "Fuel & Vehicle" once, it should suggest or automatically apply that category in the future. If the software ever guesses wrong, you can correct it and tell it to apply your choice going forward.

- Offer Smart Suggestions: For new vendors, the system can use web lookups and transaction patterns to intelligently guess the right category, complete with a confidence score and an explanation.

- Simplify Reconciliation: The software should automatically match deposits to invoices and payments to bills, flagging only the exceptions for your review.

After a couple of manual categorizations, Wesley Ledger automates more than 95% of your transactions to be categorized automatically. This frees you up from spending nights staring at spreadsheets and receipts.

Get Started in 10 Minutes

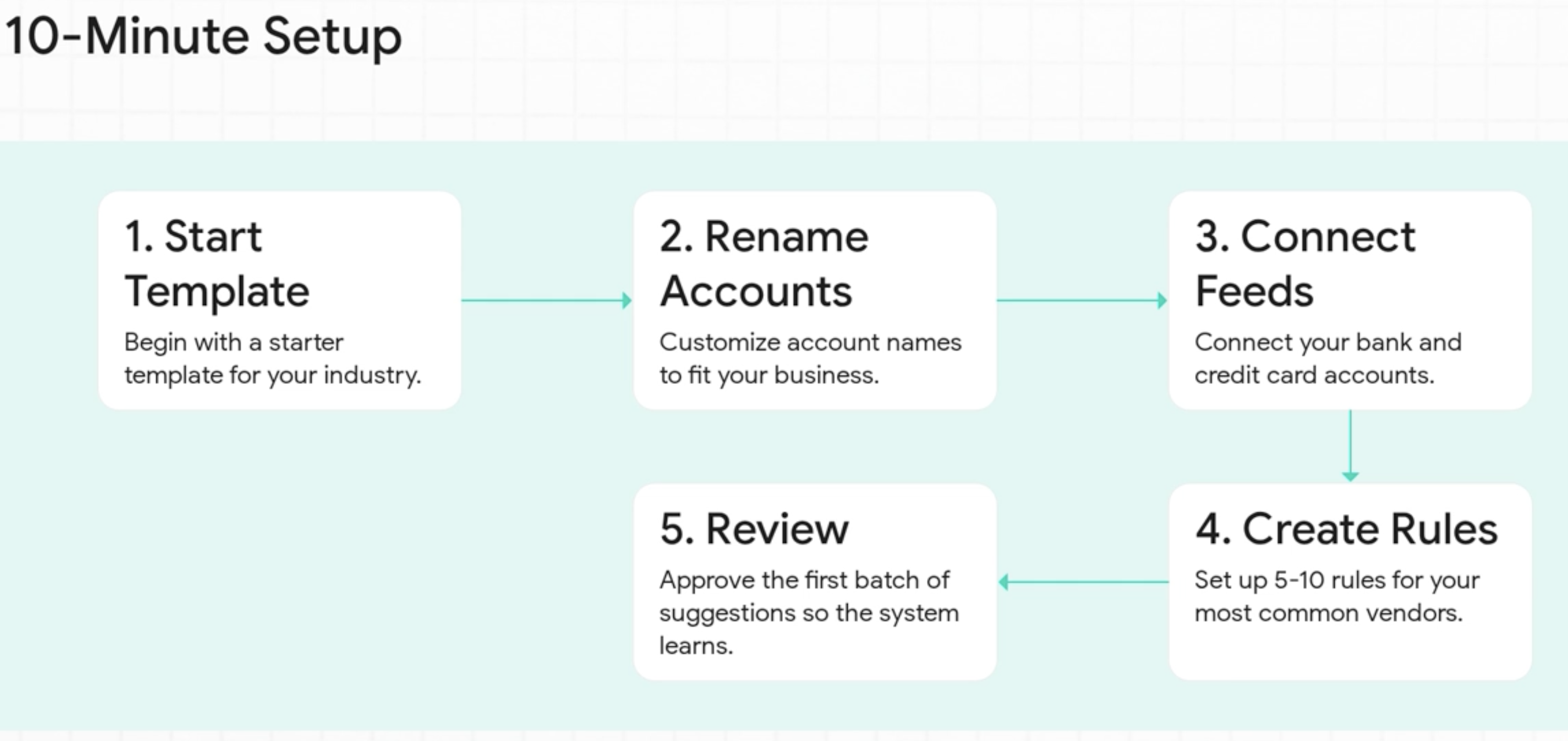

Ready to take control of your books? Here’s a quick setup guide:

- Start with a basic COA and customize it for your industry.

- Connect your bank and credit card accounts to pull in transactions automatically.

- Create 5–10 simple rules for your most common vendors (rent, software, ads, etc.).

- Review the software's suggestions and approve them so it can learn your preferences.

- Perform a quick monthly review to ensure everything is categorized and reconciled.

Your COA doesn’t have to be complicated. By keeping it simple and leveraging smart automation, you can get accurate books and more time to focus on what you do best—running your business.

For personalized advice on setting up your Chart of Accounts or for help getting started, please consult with your accountant or the Wesley AI support team for details.

This is it for today. Ready to start working on COA? Visit Wesley Ledger!

Quiz

-

- What is the primary purpose of a Chart of Accounts (COA) for a small business?

The COA serves as the master list of labels used to categorize every financial transaction. It helps small businesses organize money coming in and going out, making financial tracking clear and efficient.

-

- List three main categories of accounts found in a COA and provide an example for each.

Three main categories are Assets (e.g., Cash on Hand), Liabilities (e.g., Credit Card – Business), and Income (e.g., Sales – Online). These categories represent what the business owns, owes, and earns, respectively.

Glossary of Terms

- Chart of Accounts (COA): The master list of labels or categories a business uses to sort and classify every financial transaction, detailing money coming in and going out.

- Assets: What a business owns that has economic value, such as cash, bank balances, inventory, and equipment.

- Liabilities: What a business owes to others, including credit card balances, loans, and taxes payable.

- Equity: The owner's investment in the business plus any retained profits, representing the residual interest in the assets after deducting liabilities.

- Income: Money earned by the business from its sales of goods or services.

- Cost of Goods Sold (COGS): The direct costs attributable to the production of the goods sold by a company or the services provided. This includes materials, labor, and other direct expenses.

- Expenses: Costs incurred to run the business that are not directly tied to producing goods or services, such as rent, utilities, payroll, and marketing.

- Accounts Receivable: Money owed to the business by its customers for goods or services that have been delivered but not yet paid for.

- Accounts Payable: Money owed by the business to its suppliers for goods or services received but not yet paid for.

- Sales Tax Payable: The amount of sales tax collected by the business from customers that is owed to the government.

- Owner's Equity: The residual claim on the assets of the business after liabilities have been paid, representing the owner's investment and accumulated profits.

- Owner's Draws: Money or assets withdrawn by the owner from the business for personal use.

- Retained Earnings: The portion of net income that a business has chosen to reinvest in the company rather than distribute to its owners.

- Reconciliation: The process of ensuring that two sets of records (e.g., bank statements and internal accounting records) match, identifying and explaining any differences.

Coverage and resources

Open the authority pages that support this workflow.

Supported banks

See which institutions Wesley already covers and when statement fallback still matters.

Open page →

Integrations hub

See where Wesley fits before QuickBooks, Xero, QIF, Sage, and NetSuite workflows.

Open page →

Template library

Use saveable SOPs and checklists alongside the workflow pages.

Open page →

Try Wesley next

See whether this workflow fits your books

Book a demo, review the workflow with Wesley, and evaluate the fit before asking your team to change how they work.

Related reads

Discover adjacent articles without being sent to near-duplicate topics.