Introduction to Bookkeeping for Small Business

Bookkeeping_Essentials.mp4

This blog post aims to demystify bookkeeping and its core components for small business owners.

You don’t have to take notes or memorize. Just reading/watching is enough. We also have separate blog postings for topics you might want to know later.

Hey there, fellow business owner!

You’re passionate about what you do, whether it's baking cupcakes, designing websites, or walking dogs. But let's talk about something that might not spark as much joy: bookkeeping.

Even if the thought of numbers makes you want to run for the hills, understanding the basics is essential for your business's health and success. Think of it as the language your business speaks. This guide will help you understand the key concepts without the headache.

Why Bother with Bookkeeping?

Think of bookkeeping as the

dashboardfor your business, giving you a clear view of its health and direction

First things first: Why is bookkeeping so important?. It's more than just tracking money in and out. Good bookkeeping helps you understand if you're actually making a profit, allows you to make smarter business decisions, and makes tax time way less stressful. Modern accounting software like Wesley Ledger automates

Let's dive into some core ideas that will set you up for success.

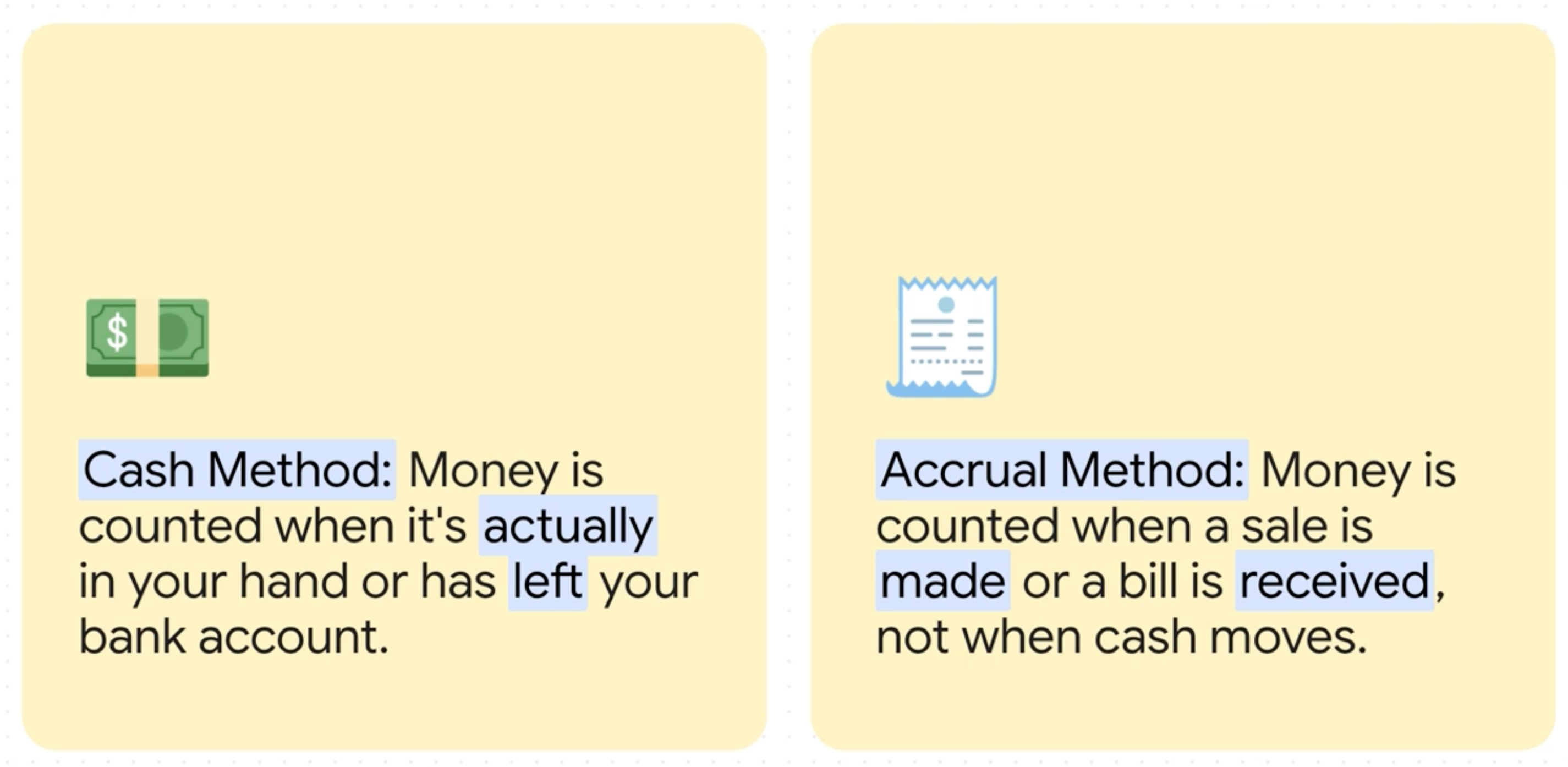

1. Cash vs. Accrual: When Do You Count Your Money?

This is one of the first big decisions you'll make. It’s all about *when* you record income and expenses.

Cash Method: This is the simple one. You record income when the cash actually hits your bank account, and you record an expense when you actually pay for it. For example, if you invoice a client in January but they don't pay you until February, you record that income in February.Accrual Method: This method records income when you earn it (like when you send the invoice) and expenses when you incur them (like when you receive a bill), regardless of when money changes hands. It can give you a more accurate picture of your profitability over time.

For many small businesses, the cash method is often easier to start with. However, accrual method is going to give you a more accurate picture if you are selling credit and inventory.

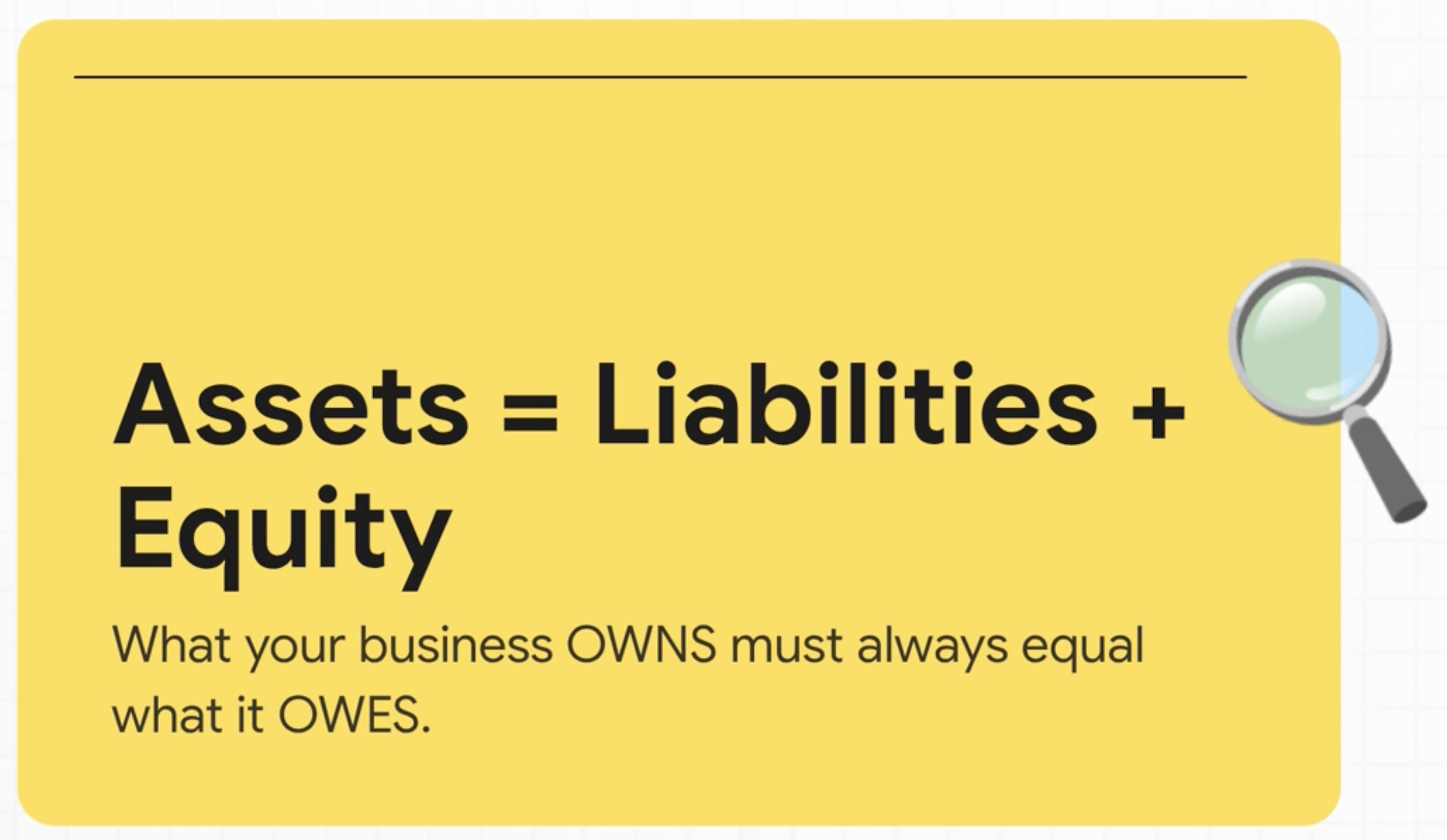

2. The Core of Accounting: The Accounting Equation

Everything in bookkeeping boils down to one simple formula:

Assets = Liabilities + Equity

Let's break that down with a friendly example. Imagine you run a small coffee cart:

- Assets: These are the things your business owns that have value. For your coffee cart, this would be your espresso machine, the cart itself, and the cash in your register.

- Liabilities: This is what your business owes to others. Maybe you took out a small loan to buy that espresso machine. That loan is a liability.

- Equity: This is what's left over for you, the owner. It’s the value of your assets minus what you owe to others.

This equation must always be in balance, which leads us to our next point. If you want more examples tailored to your business, you can connect your accounts to Wesley Ledger and ask questions. Here is the link

3. Double-Entry, Debits & Credits (Simplified!)

https://www.youtube.com/watch?v=cjO8qHM5Wjg

This might sound intimidating, but the concept is straightforward. For every transaction, there are always at least two entries: a debit and a credit. This system ensures the accounting equation stays balanced.

Think of it like this: If you buy a new grinder for your coffee cart (an asset), the cash in your bank account (another asset) goes down. One account goes up, and another goes down. That's the essence of double-entry bookkeeping.

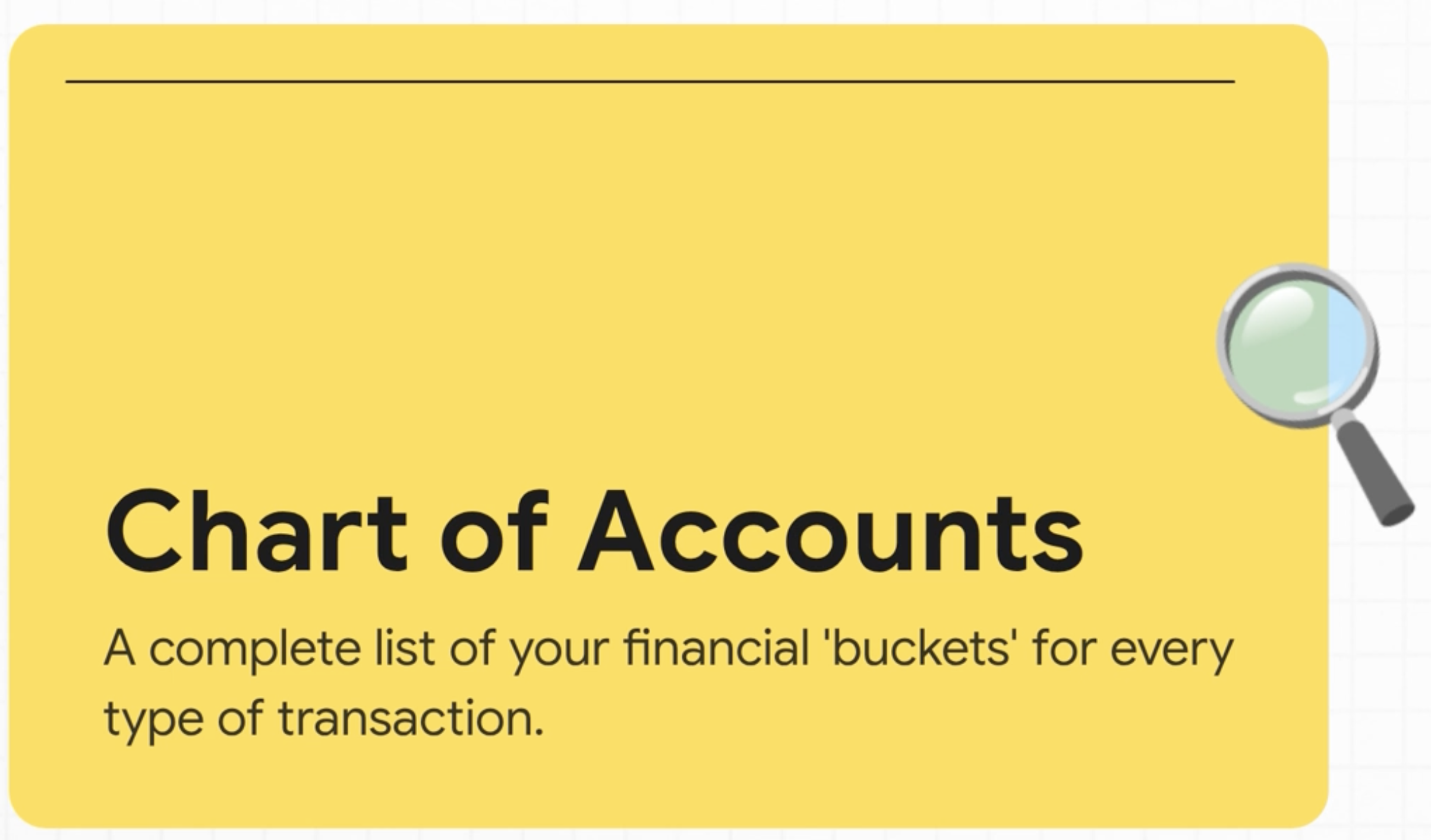

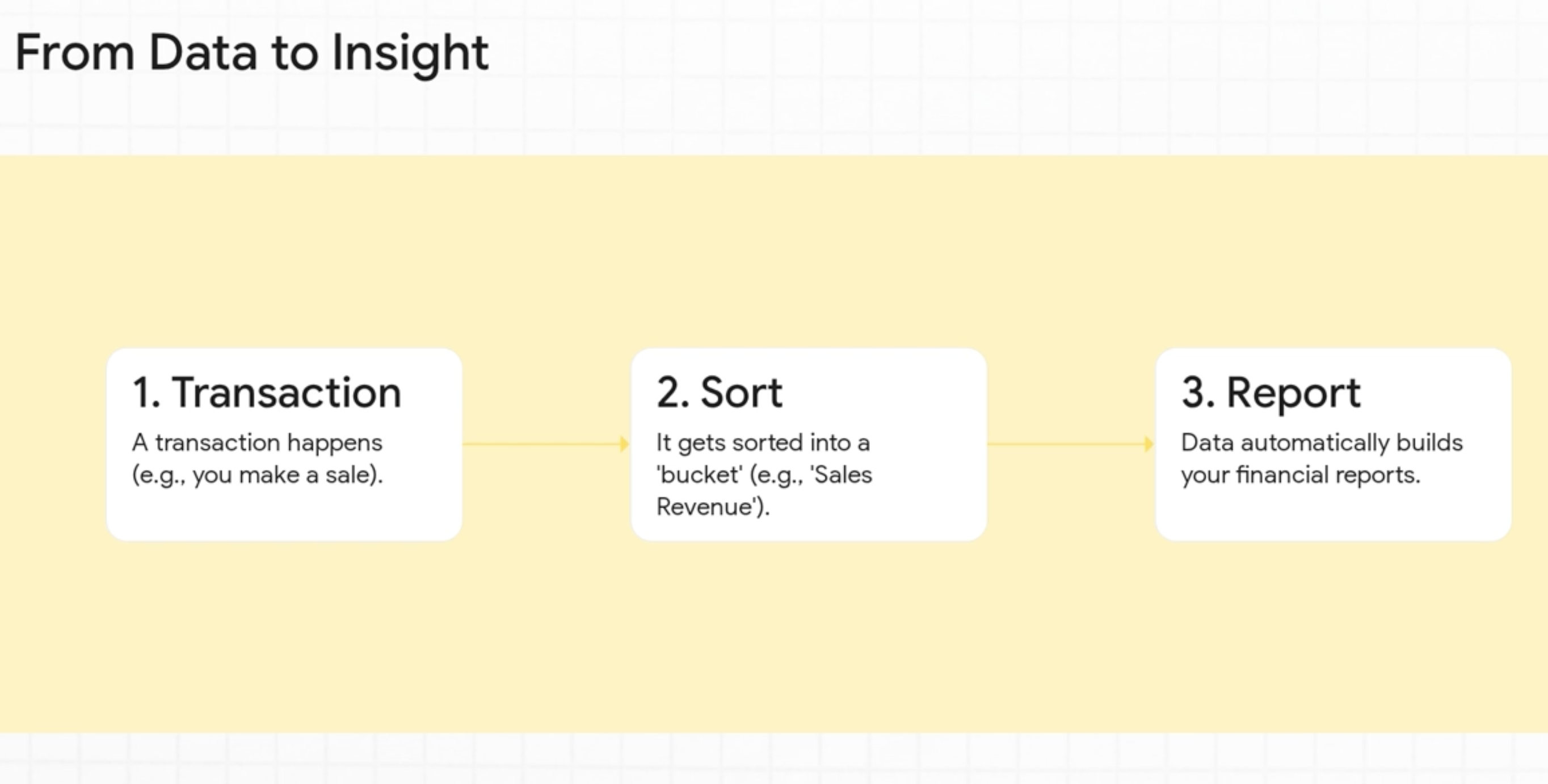

4. Organizing Your Money: The Chart of Accounts

Imagine you have a bunch of buckets to sort your money into. That's your Chart of Accounts! It’s just a list of all the categories you use to track your transactions, like "Coffee Bean Sales," "Office Supplies," "Marketing Expenses," and "Equipment". Setting this up correctly from the start makes everything easier to manage.

5. Your Business Report Cards: Financial Statements

Finally, all this hard work comes together in a few key reports that tell you how your business is doing.

- Profit & Loss (P&L) Statement: Also called an Income Statement, this report shows you how profitable your business was over a period of time (like a month or a quarter). It lists your income and subtracts your expenses to show your net profit or loss.

- Balance Sheet: This is a snapshot of your business's financial health at a single moment in time. It shows what you own (assets), what you owe (liabilities), and what's left (equity), proving that the accounting equation is, in fact, balanced.

- Cash Flow Statement: This statement tracks all the cash coming in and going out of your business. It's super important for understanding if you have enough cash on hand to pay your bills.

This is it for today. Taking the time to understand these basics will empower you to build a stronger, more successful business. You've got this!

Quiz

-

- What is the primary benefit of bookkeeping, even for individuals who find it unappealing?

Bookkeeping provides essential financial insights into a business's health and performance. It allows businesses to track income and expenses, manage cash flow, and make informed decisions, even if the process itself is not enjoyable.

-

- Briefly explain the difference between cash basis and accrual basis accounting.

Cash basis accounting recognizes revenues and expenses when cash is actually received or paid, while accrual basis accounting recognizes them when they are earned or incurred, regardless of when the cash transaction occurs.

-

- What is the fundamental principle behind double-entry bookkeeping?

The fundamental principle of double-entry bookkeeping is that every financial transaction affects at least two accounts. This ensures that the accounting equation remains balanced and provides a complete record of financial activity.

-

- State the Accounting Equation and identify what each component represents.

The Accounting Equation is Assets = Liabilities + Equity. Assets are what a business owns, Liabilities are what it owes, and Equity is the owner's stake in the business.

-

- What is the purpose of a Chart of Accounts?

A Chart of Accounts is a categorized list of all the accounts used by a business to record its financial transactions. It provides a standardized framework for organizing and reporting financial data.

-

- Name the three primary financial statements discussed in the "Bookkeeping Essentials" source.

The three primary financial statements discussed are the Profit & Loss (Income Statement), the Balance Sheet, and the Cash Flow Statement.

Coverage and resources

Open the authority pages that support this workflow.

Supported banks

See which institutions Wesley already covers and when statement fallback still matters.

Open page →

Integrations hub

See where Wesley fits before QuickBooks, Xero, QIF, Sage, and NetSuite workflows.

Open page →

Template library

Use saveable SOPs and checklists alongside the workflow pages.

Open page →

Try Wesley next

See whether this workflow fits your books

Book a demo, review the workflow with Wesley, and evaluate the fit before asking your team to change how they work.

Related reads

Discover adjacent articles without being sent to near-duplicate topics.