Cash Flow Statement For Small Business

Understanding_Cash_Flow.mp4

Ever wonder why your Profit & Loss (P&L) statement shows a great profit, but your bank account feels a little… light? You're not alone! This common puzzle is why understanding your Cash Flow Statement is so crucial for any small business owner.

Think of your Cash Flow Statement as the real story of your money – where it actually came from and where it actually went during a specific period, like last month or quarter. Unlike the P&L, which might include invoices you haven't been paid for yet, the cash flow statement focuses solely on the real money moving in and out of your bank and pocket.

It’s divided into three clear sections, each telling a different part of your financial story:

1. Operating Activities: Running the Day-to-Day Business

This section is all about your core business operations. It includes the daily cash coming in from customer payments and the cash going out for things like paying suppliers, wages, rent, utilities, and taxes.

- Why it matters: This tells you if your main business activities are generating enough cash on their own. If this number is consistently negative, it means you're likely funding your day-to-day costs with loans or your own savings.

Examples: Customer receipts (+$12,000), paying for coffee beans (–$4,500), wages (–$3,000), rent (–$1,200), taxes (–$300).

2. Investing Activities: Building Your Business for the Future

This section tracks cash related to buying or selling long-term assets that help your business grow. This includes things like new equipment, vehicles, computers, or lease deposits.

- Why it matters: Seeing cash go out here isn't necessarily "bad" – it often signifies growth! However, big purchases can significantly lower your cash now, so it’s essential to plan for them.

Example: Buying a new espresso machine (–$2,200).

3. Financing Activities: Funding and Owner Contributions

This final section deals with the money exchanged between your business, its owners, and lenders. This covers things like receiving loans, repaying loan principal, owner contributions to the business, or owner draws (money you take out).

- Why it matters: Financing can be useful for bridging cash gaps. Just be sure to keep a close eye on loan repayments and interest, as these can squeeze your future cash flow.

Examples: Owner adds money to the business (+$1,000), loan repayment (principal only) (–$400).

The Big Picture: Why Your Cash Flow Statement is a Lifesaver

Understanding these three sections helps you avoid common small business pitfalls:

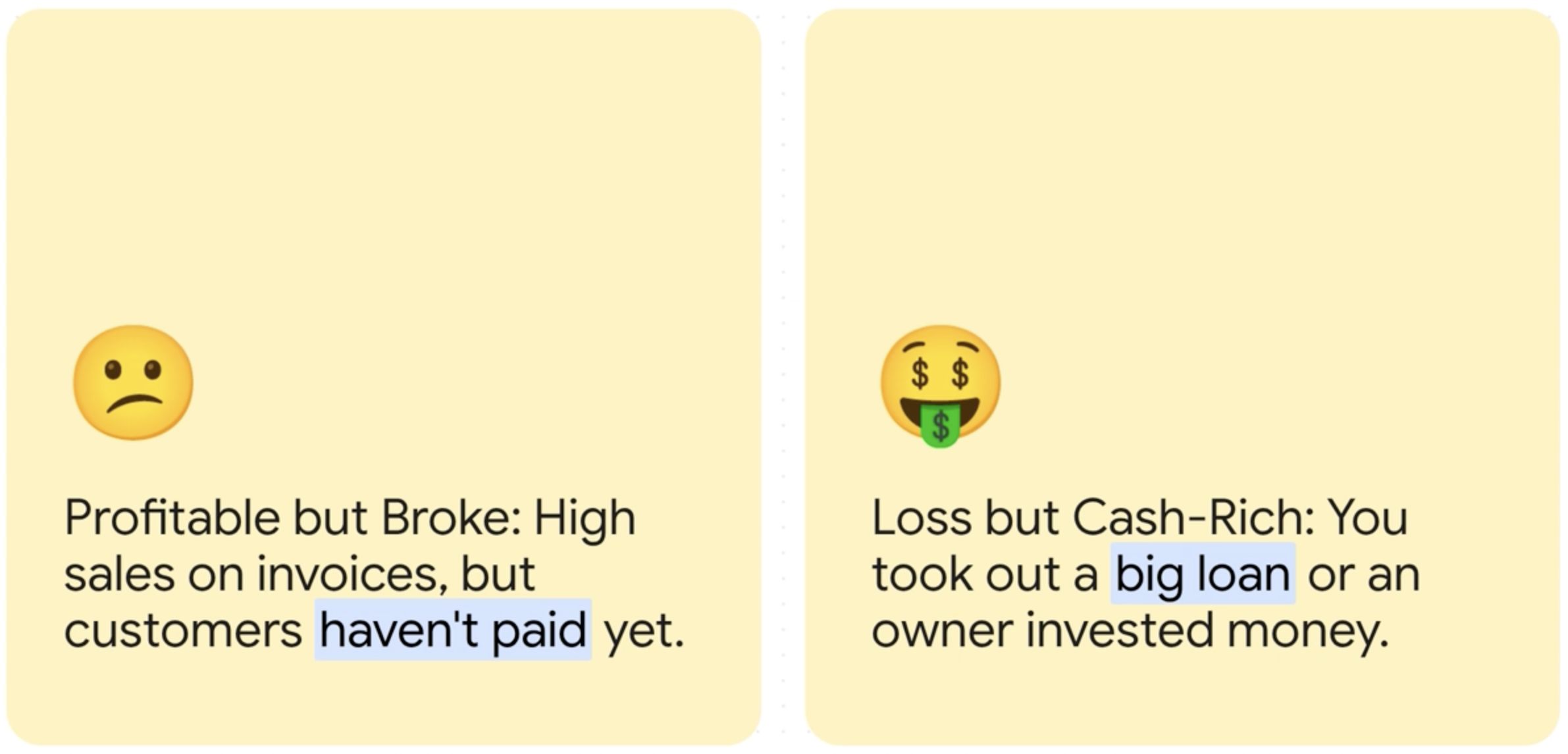

- Profitable but Broke: Your P&L might show profit, but if customers haven't paid their invoices yet (meaning your Accounts Receivable increased), your operating cash flow could be negative. The cash flow statement shows you this reality.

- Loss but Cash-Rich: You might have taken a loss on paper, but if you received a large loan or made an owner contribution, your financing cash flow would be positive, making your cash balance look healthy.

- Seasonal Swings: The cash flow statement makes it clear when you have strong cash months, allowing you to plan to fund weaker months.

How Modern Accounting Software Makes it Easy

Wesley gathers your transactions and creates cash flow statement with a click of a button.

Gone are the days of complex spreadsheets! Accounting software can dramatically simplify managing your cash flow:

- Automated Tracking: It can automatically pull bank and credit card transactions and help categorize them into operating, investing, or financing activities using rules you set.

- Clarity on Cash vs. Accrual: It helps you see actual cash movements separately from your P&L, clarifying why profit isn't always equal to cash.

- Loan Management: Software can automatically split loan payments into principal (financing) and interest (operating).

- Forecasts & Alerts: Many tools can forecast future cash based on upcoming bills and invoices, and even warn you if your cash might go negative.

Quick Starter Checklist for Better Cash Flow

Ready to get a clearer picture of your money?

- Connect all your bank and credit accounts to your accounting software.

- Create rules for frequent vendors (e.g., "payments to BeanCo → Operating: Supplies") to automate categorization.

- When you buy big items like equipment, mark them as assets (investing), not just expenses.

- Set up your loans properly so principal and interest are split correctly.

- Review your operating cash flow monthly – aim for it to be positive and trending up.

- Use a 90-day cash forecast to plan big purchases and loan repayments.

By paying attention to your cash flow statement, you'll gain invaluable insights into your business's true financial health and make smarter decisions for sustainable growth!

Choose your workflow

Bank statement to CSV converter

Start from the general statement-conversion workflow.

PDF to CSV converter

Use the broad PDF-to-CSV workflow for statement and document cleanup.

Bank statement conversion hub

The full cluster for PDF, CSV, OCR, and review-first statement workflows.

Import bank statements into QuickBooks Online

QBO upload path for PDF, image, QBO, QFX, and CSV statement files.

Convert a bank statement PDF to CSV for free

Best for one-off statement cleanup and quick spreadsheet-ready exports.

Coverage and resources

Open the authority pages that support this workflow.

Supported banks

See which institutions have dedicated coverage pages and where statement fallback still makes sense.

Open page →

Supported statement types

See which source documents Wesley can clean up before export or import prep.

Open page →

Bank Statement Cleanup SOP for Bookkeepers

A bank statement cleanup SOP for bookkeepers who need a repeatable review process before exporting to QuickBooks, Xero, QIF, or spreadsheet workflows.

Open page →

Ready to use the matching workflow?

Bank statement to CSV converter

Start from the general statement-conversion workflow.

Related reads

Discover adjacent articles without being sent to near-duplicate topics.