Balance Sheet: Financial Selfie of your business

The_Balance_Sheet_Snapshot.mp4

Ever wish you had a quick snapshot of your business's financial health? That's exactly what a Balance Sheet is! It's like a financial selfie, showing where your business stands at a specific moment in time – for example, "as of September 30". For small business owners, understanding this report is crucial, and it's simpler than you might think!

What's Inside Your Financial Selfie?

The Balance Sheet is built on a fundamental, unbreakable rule: Assets = Liabilities + Owner’s Equity. Let's break down these three core parts:

Assets – What You OWN

These are all the valuable things your business possesses. Think of them as everything that could put money in your pocket, or that helps you make money.

| Cash & Bank | The money readily available in your accounts. |

|---|---|

| Accounts Receivable (A/R) | Money customers owe you for products or services they've already received. |

| Inventory | Items you plan to sell, or the ingredients/supplies you use to create them. |

| Fixed Assets | Larger, long-term items like equipment, vehicles, or furniture, recorded at their cost minus depreciation |

Liabilities – What You OWE

These are your business's financial obligations – the money you need to pay out to others.

| Accounts Payable ( A/P ) | Bills from suppliers or vendors that you haven't paid yet. |

|---|---|

| Credit Cards / Short-Term Loans | Debts that are due relatively soon. |

| Long-Term Loans | Larger debts, like a bank loan, that you'll repay over a year or more. |

Owner’s Equity – What’s Left for YOU

This is your stake in the business – what would be left if you sold all your assets and paid off all your liabilities. It includes money you've invested (Contributed Capital) and the accumulated profits the business has kept (Retained Earnings or Retained Profit).

Why Does Your Balance Sheet Matter?

In just a few seconds, your Balance Sheet can tell you a lot:

- Can you pay your bills? (

Liquidity) It shows if you have enough readily available assets to cover upcoming payments. - How much debt are you carrying? (

Leverage) It reveals your total debt load compared to your assets. - What's your business worth? (

Net Worth) Your Owner's Equity is essentially your business's net worth. Watching this grow typically signals improving health.

A Quick Example: Coffee Cart LLC

Let's look at a simplified example for "Coffee Cart LLC" as of September 30:

Assets (What they own):

| Cash | $12,000 |

|---|---|

| Accounts Receivable | $5,000 |

| Inventory | $8,000 |

| Equipment ( Net ) | $16,000 ( $20,000 - $4,000 ) |

| Total Assets | $41,000 |

Liabilities (What they owe):

| Credit Card Payable | $3,000 |

|---|---|

| Accounts Payable | $6,000 |

| Bank Loan | $20,000 |

| Total Liabilities | $29,000 |

Owner's Equity (What's left for the owner):

| Contributed Capital | $10,000 |

|---|---|

| Retained Profit to date | $2,000 |

| Total Equity | $12,000 |

Check the Balance: Assets $41,000 = Liabilities $29,000 + Equity $12,000. It balances!

How to "Read" Your Balance Sheet Quickly

You don’t have to remember the numbers. Because Wesley will do it for you!

You don't need to be an accountant to get valuable insights:

Current Ratio: This tells you if you have enough short-term assets (like Cash, A/R, Inventory) to cover your short-term bills (like Credit Card Payable, A/P).- For Coffee Cart LLC, Current Assets ($25k) / Current Liabilities ($9k) = ~2.78. A ratio around 1.5 or higher is generally considered healthy, meaning you have more short-term assets than debts.

Quick Ratio: Similar to the current ratio, but it removes inventory. This shows if you can pay your immediate bills without having to sell your products first.- For Coffee Cart LLC, Quick Assets ($17k) / Current Liabilities ($9k) = ~1.89, which is also strong.

Debt Load: Compare your Total Debt to your Total Assets. If debt is growing faster than your assets or equity, it could be a red flag.- Coffee Cart LLC has $29k in debt versus $41k in assets, meaning about 71% of its assets are financed by debt and payables.

Owner's Equity Trend: Is your equity going up month-over-month? Rising equity usually means your business is becoming more valuable and financially healthier!

How the Balance Sheet Changes

The Balance Sheet is dynamic! Every transaction impacts it while keeping the core formula in balance:

- You buy inventory with a credit card: Inventory (Asset) goes up, Credit Card (Liability) goes up. The balance remains.

- A customer pays an invoice: Cash (Asset) goes up, Accounts Receivable (Asset) goes down. Total assets remain the same, but your cash position improves.

- You earn profit: Cash, Receivables, or Inventory may rise, and your Equity (Retained Earnings) definitely increases.

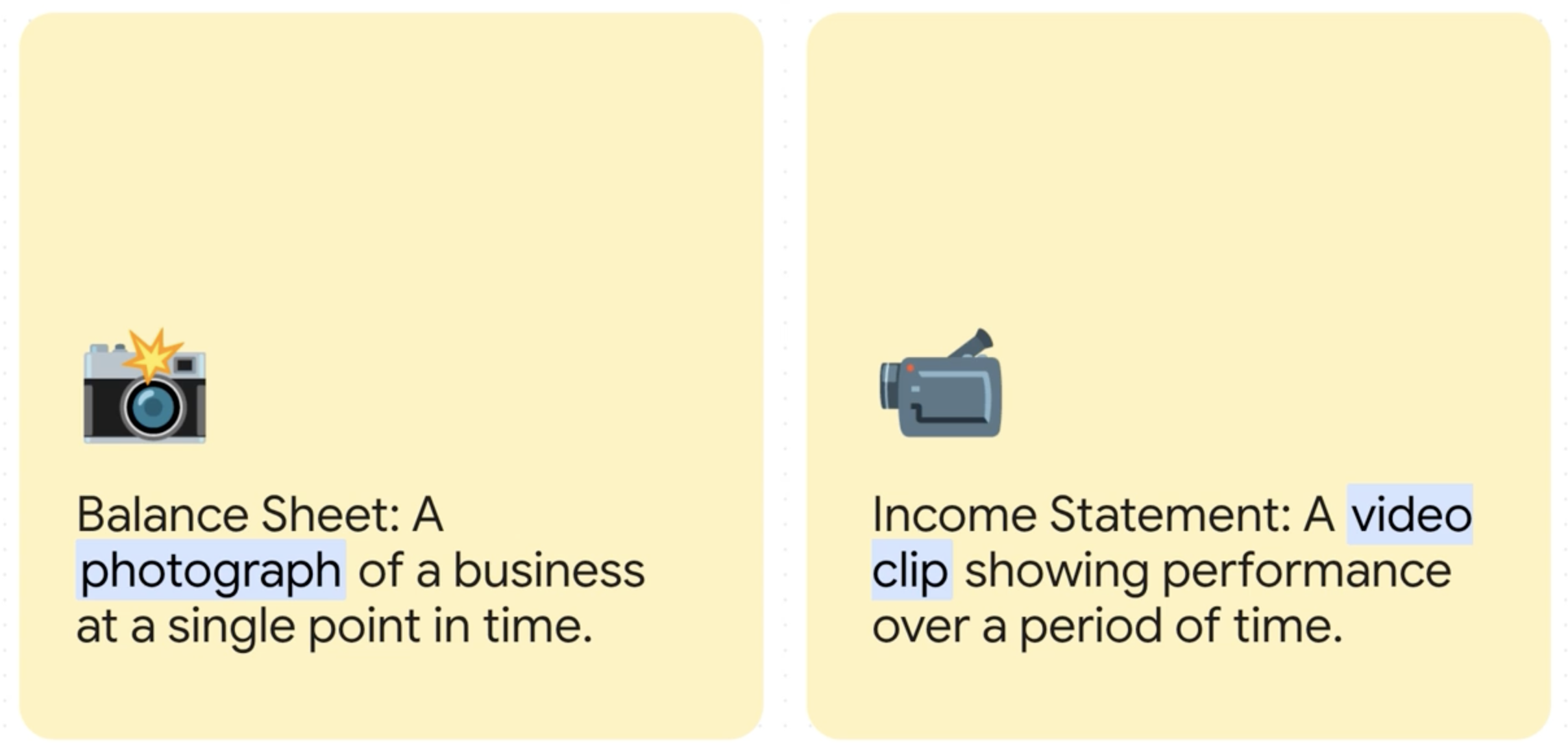

Balance Sheet vs. Income Statement

It's easy to confuse them, but they serve different purposes:

Balance Sheet: A snapshot of your financial position at one specific point in time (e.g., "as of September 30").Income Statement: Covers a period of time (e.g., "for the month of September"), showing your revenues minus expenses to calculate profit.

Making It Easier with Accounting Software

Don't panic about tracking all these numbers manually! Modern accounting software can be a huge help:

- Automated Data: Connects to your bank and credit cards to keep your Cash, A/R, and A/P up-to-date daily.

- Smart Categorization: Helps classify transactions correctly, reducing errors.

- One-Click Reports: Generates key reports and ratios like Current Ratio and debt-to-equity with ease.

Your Simple Checklist for Success

If you want to run a health-check for your business, answer these 5 questions.

As a small business owner, regularly ask yourself:

- Do I have enough current assets to cover my current liabilities (aim for a current ratio of 1.5 or higher)?

- Is Accounts Receivable piling up? (Maybe tighten up collections.)

- Is my inventory too high, tying up cash?

- Is my debt growing faster than my assets or equity?

- Is my Owner's Equity trending upward month-over-month?

By regularly reviewing your Balance Sheet, you gain powerful insights into your business's financial health, helping you make smarter decisions and steer your company toward success!

Want to let software do the finance and focus on growth? Try Wesley!

Coverage and resources

Open the authority pages that support this workflow.

Supported banks

See which institutions Wesley already covers and when statement fallback still matters.

Open page →

Integrations hub

See where Wesley fits before QuickBooks, Xero, QIF, Sage, and NetSuite workflows.

Open page →

Template library

Use saveable SOPs and checklists alongside the workflow pages.

Open page →

Try Wesley next

See whether this workflow fits your books

Book a demo, review the workflow with Wesley, and evaluate the fit before asking your team to change how they work.

Related reads

Discover adjacent articles without being sent to near-duplicate topics.